The Children’s Health Insurance Program (CHIP), passed on a bipartisan manner and signed into law in 1997, remains a model of health care coverage that works. With eight million children covered throughout the year, CHIP provides the child-specific benefits and affordability that families want and need for their children. While the Affordable Care Act (ACA) Marketplaces also offer Qualified Health Plans (QHPs) under which children can be covered, a review of those plans, as compared to CHIP, shows that they lack child-specific benefits and cost substantially more in terms of out-of-pocket fees.

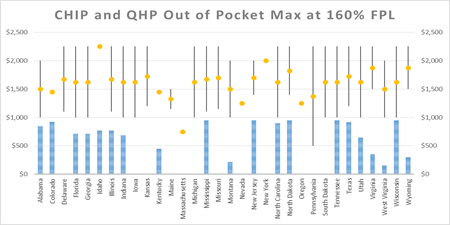

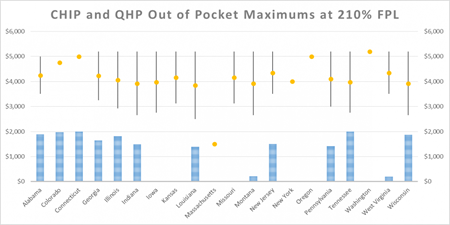

Wakely Consulting group completed the study: Comparison of Benefits and Cost Sharing in Children’s Health Insurance Programs to Qualified Health Plans, for the Robert Wood Johnson Foundation. It compares the cost sharing in CHIP plans and QHPs in thirty five states for families living at 160% of the Federal Poverty Level (FPL) and at 210% FPL. The review includes a look at the average user in a CHIP or QHP plan as well as the maximum out-of-pocket costs for a child with special health care needs. The analysis also reviewed the specific benefits that offered under CHIP plans and QHPs.

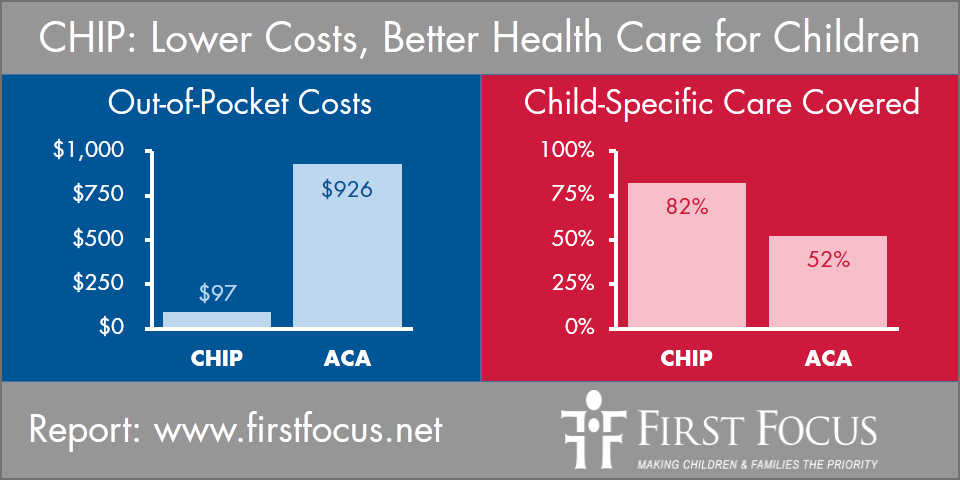

The graph below shows how CHIP and QHPs stack up when it comes to cost-sharing and child specific services.

Cost-sharing Comparisons

The study shows that CHIP enrollees who transition to a QHP would see a substantial increase in out-of-pocket costs at the point of care. The average out-of-pocket costs for a child in a QHP, at 160% FPL, is $446 a year. If that same child was in CHIP, the average out-of-pocket costs on a yearly basis would be $66. At 210% FPL, the increase in costs go from an average of $97 annually for a child on CHIP, or $926 as the annual average for a child in a QHP.

In all states included in the analysis and at both income levels, the out-of-pocket maximum in QHPs far exceeds that in the CHIP plans. That increase in costs is especially pronounced for children with special care needs who may have to seek medical help on a regular or frequent basis and who will likely reach the out-of-pocket maximum for cost sharing in a year. In all states reviewed by Wakely, the out-of-pocket maximum costs in QHPs far exceeds that of CHIP. In some states, children with special health care needs could go from paying $0 in CHIP to over $5,000 in annual out-of-pocket expenditures in QHPs. All states included in the analysis had lower maximum out-of-pocket costs in CHIP compared to QHPs. The lowest combined medical and prescription drug out-of-pocket maximum costs for QHPs across the states was $500 for families with household incomes of 160% FPL, and $2,250 for families with household incomes of 210% FPL. Families who have children with special health needs could face daunting out-of-pocket costs in QHPs above and beyond any premiums that must be paid.

Reviewing Benefits

The differences between CHIP and QHPs continue when benefits are taken into account. The core services in CHIP and the QHPs are very similar because the QHPs are based on the required Essential Health Benefits (EHB). But, when the child-specific benefits are reviewed, CHIP comes out ahead in terms of which benefits are offered, cost-sharing, and imposing fewer limits. The report looks at these child-specific services:

- Dental – Preventive and Restorative and Orthodontics

- Vision – Exams and Corrective Lenses

- Audiology – Exams and Hearing Aids

- Autism – General Services

- Applied Behavior Analysis Therapy

- Habilitation

- Physical Therapy, Occupational Therapy, and Speech Therapy

- Enabling Services

- Medical Transportation – Non-Emergency Transportation

- Over-the-Counter Medications

The review of these benefits in the 35 states show that CHIP plans include coverage of these child-specific benefits much more frequently than QHPs. For the services that are covered, QHPs tend to include more limits on the services.

Congress Must Continue CHIP Funding for States

While the ACA holds great promise for the millions of Americans who have lacked an affordable coverage option, especially uninsured adults, more work is needed to be sure that new coverage options, eligibility rules, enrollment systems, policies and procedures, benefits, plans and provider networks are able to meet the unique health and developmental needs of children. This analysis shows that CHIP must remain intact as Marketplace coverage matures to be sure we don’t lose ground on our nation’s unprecedented success in covering children.

CHIP is a cost-effective, common-sense approach to coverage that has reduced the numbers of uninsured children to record lows, even during the economic crisis that began in 2008. Children must continue to have access to stable coverage through proven programs like CHIP until it is clear that there is a comparable alternative. First Focus urges Congress to extend CHIP funding for four years to ensure that children’s coverage remains strong. If Congress does not extend CHIP funding beyond the current September 30, 2015 expiration, important gains for children will be lost. Now is not the time to disrupt the coverage that is working for children.

Download our summary of the study here.

Read the press release here.